This is 2022 in a nutshell: More people are saving for retirement, but few are saving enough.

Every year, Vanguard publishes a report on the state of the nation’s retirement savings habits. Participation rates among workers with access to 401(k) plans have surged from 72 percent in the past five years to 83 percent in 2022, according to the report. Latest report 401(k) plans in Vanguard’s large customer base.

It is to some credit that automatically enrolling employees in their plans is becoming more popular among employers. Under this company policy, he has a 93% employee participation rate in 401(k)-style plans, but only 70% when he can’t get that kind of encouragement and has to decide for himself whether to save. A growing number of states are also requiring employers to set up her 401(k) plan in-house or automatically enroll workers in state-backed IRAs, which may also have a modest effect on savings.

But a closer look at the Vanguard data reveals a divide between the haves and the have-nots. High-income participation is very high, but low-income participation is lagging behind. Research shows that national IRA programs are reaching more low-wage workers. Still, according to Vanguard, only about half of those with incomes under $30,000 saved more than 90% of those with incomes above $100,000 last year.

But even workers who regularly put money into their 401(k) accounts aren’t saving enough, and last year’s stock market sell-off did a lot of damage.

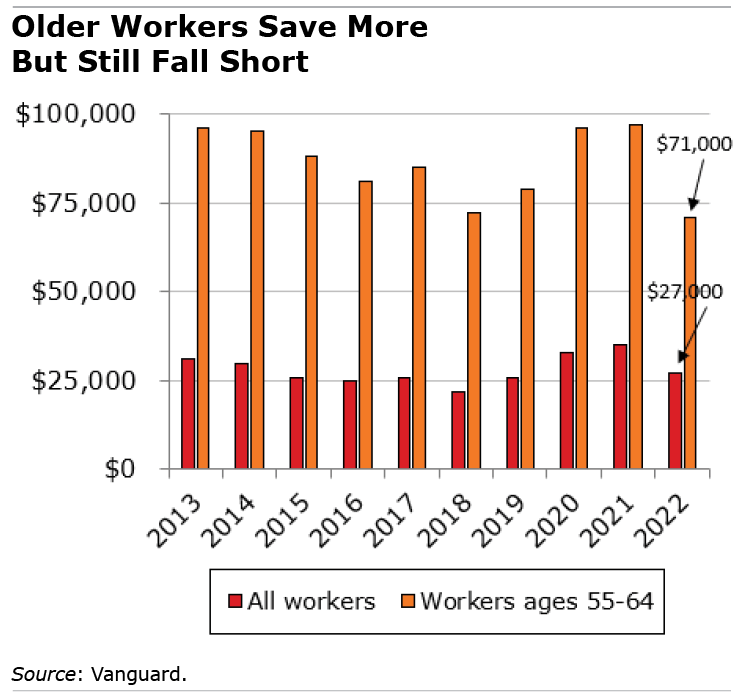

The Standard & Poor’s 500 Market Index is down nearly 20% in 2022, dropping the typical worker’s 401(k) balance to just $27,400. This is down from the already low level of $35,300 in 2021. Ten years ago, the equivalent balance was $2,000 higher than he was.

To be fair, the stock market has rebounded nicely this year. And 2022’s small balance is an inaccurate gauge of the state of the American public, as it includes workers who are just beginning their careers and those who have just started saving through state IRA programs and still have small account balances. A worker in Vanguard data may have money on her 401(k) from an IRA or former employer, or her spouse may have her 401(k).

So let’s take a look at the aging workforce, who should be preparing a lot of retirement money by now.The typical worker aged 55 to 64 who is on the runway to retirement is just $71,000 in 401(k). That’s the lowest for that age group in more than a decade of Vanguard data, and no more than a few hundred dollars a month in retirement income.

Let’s hope Vanguard’s 2023 report is better – and it may be. According to Vanguard, four in 10 workers are spending a greater percentage of their paycheck on their 401(k), and a rising stock market will help workers make ends meet.

It’s going to be hard to get any worse than 2022.

square away Writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC.How to stay up to date please blog joining our free email list. You will only receive one email each week with links to his two new posts for the week. sign up here. This blog is supported by the Boston University Center for Retirement Studies.